VER’s return on investment 8.2% during 1 Jan–30 June 2019; ten-year average annual return 6.7%

Published 2019-08-23 at 10:39

INVESTMENT ENVIRONMENT

The first half of 2019 was favourable for the investment market. The market recovered quickly in January after the bleak last weeks of 2018, and the fall in prices experienced in May proved short-lived.

Overall developments in the interest rate markets were also favourable as general interest rates declined while at the same time many risk premiums narrowed.

Underlying the positive market developments were the monetary policies pursued by central banks and the expectations regarding future monetary policy. Primarily for these reasons, the stock markets and risky interest rate markets weathered well in the face of the weakening economic growth and less optimistic macro-economic forecasts.

VER’S RETURNS ON INVESTMENTS

Future monitoring and evaluation of the State Pension Fund’s investment activities will increasingly focus on long-term outcomes and future prospects instead of quarterly reporting. However, VER will continue to post quarterly figures and comments to the same extent as previously.

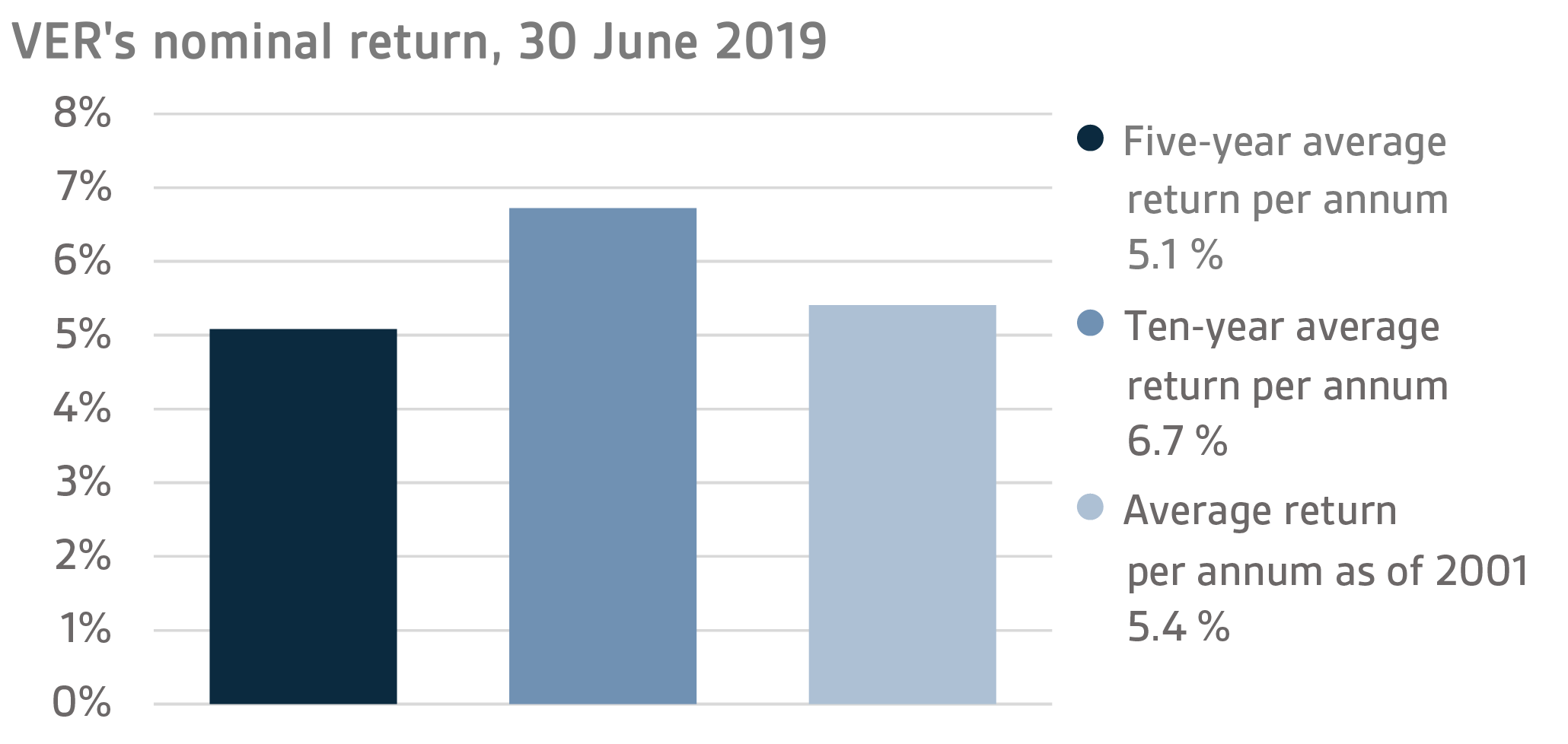

On 30 June 2019, VER’s investment assets totalled EUR 19.7 billion. During the first half of the year, the return on investments at fair values was 8.2 per cent. The average nominal rate of return over the past five years (1 July 2014–30 June 2019) was 5.1 per cent and the annual ten-year return 6.7 per cent. Since 2001, when VER’s activities assumed their current form, the average rate of return has been 5.4 per cent.

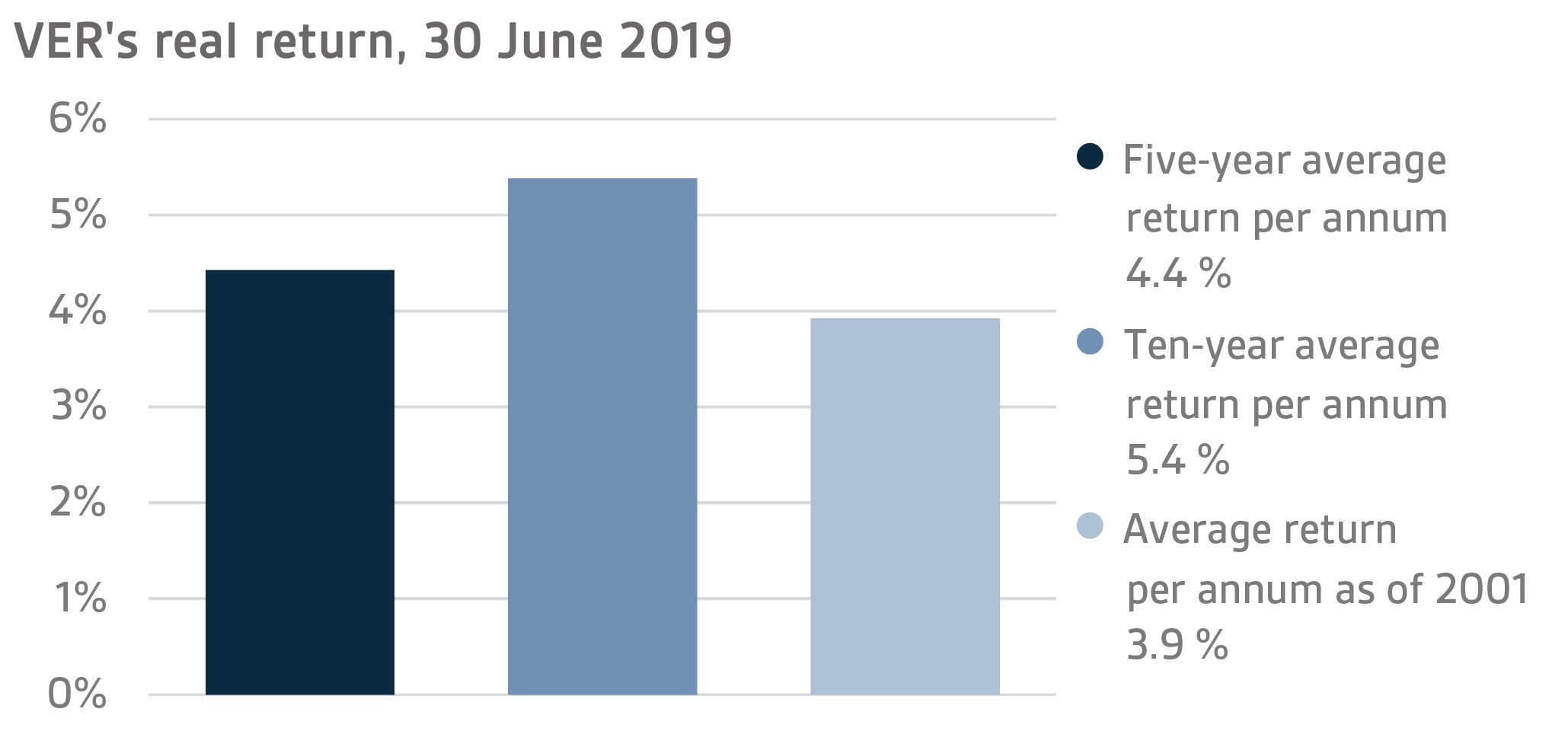

The real rate of return during the first half of 2019 was 7.5 per cent. VER’s five-year average real return was 4.4 per cent and ten-year real return 5.4 per cent.

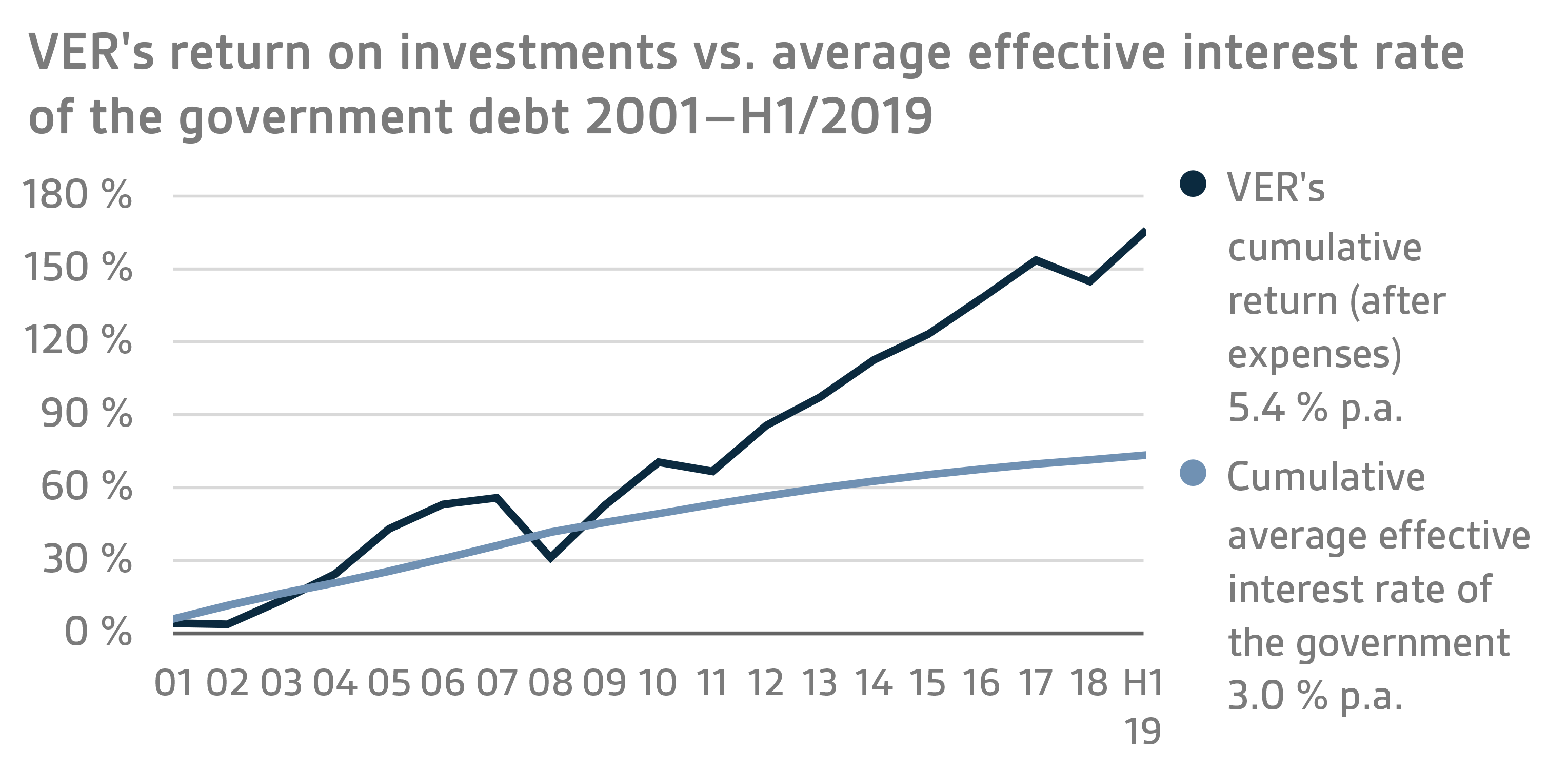

From the state’s point of view, it is pertinent to compare the return on investments with the cost of net government debt, because the funds accumulated in preparation for future pension expenditure can be deemed to reduce such debt. Over the past ten years, VER’s average annual rate of return has beaten the cost of net government debt by 4.5 percentage points. Since 2001, the total market-value returns earned by VER have exceeded the cumulative average cost of equivalent government debt by about EUR 6 billion over the same period.

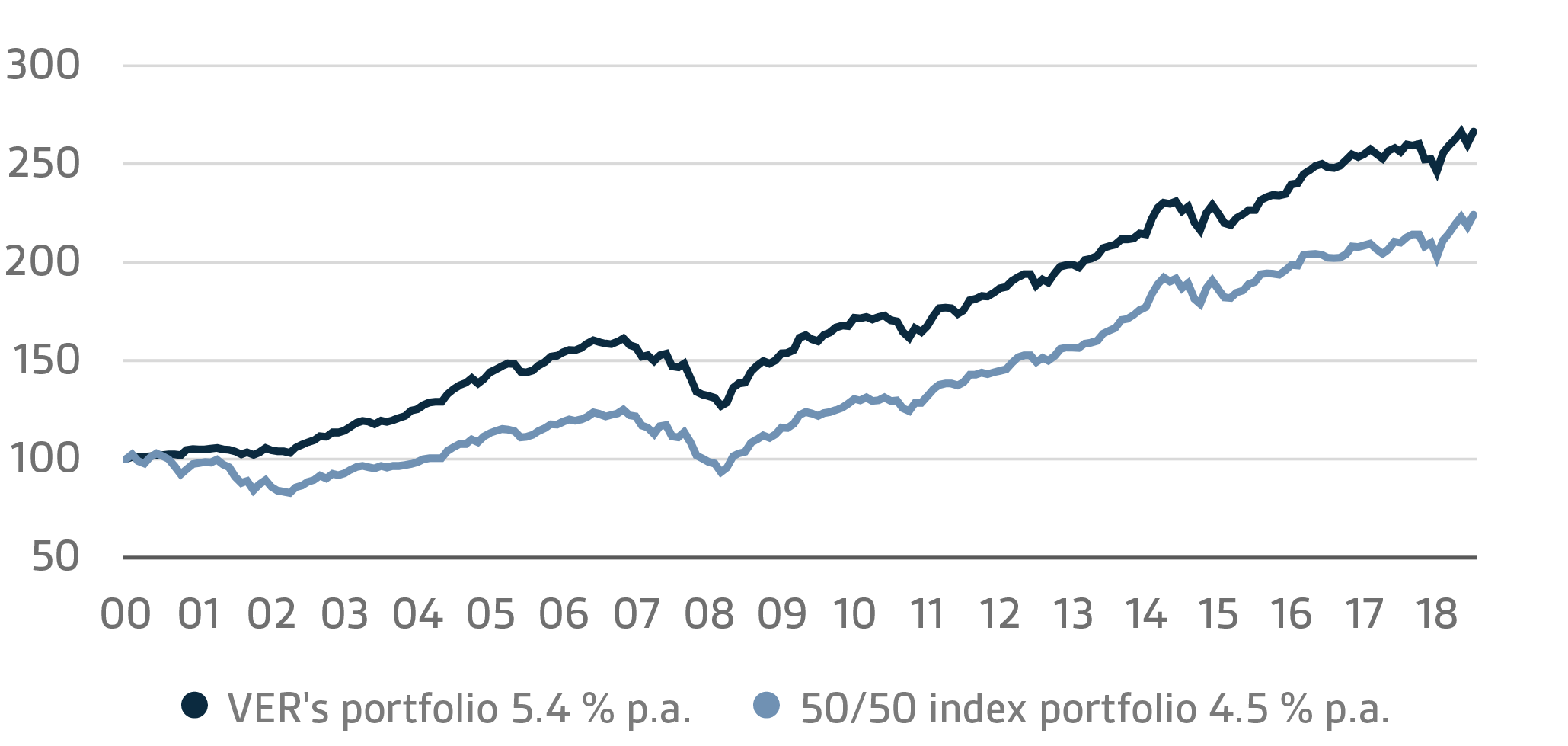

VER monitors long-term return relative to overall market developments by comparing the actual return with a global index, in which the weight of both equities and currency-hedged bonds is 50 per cent.

A CLOSER LOOK AT JANUARY–JUNE 2019

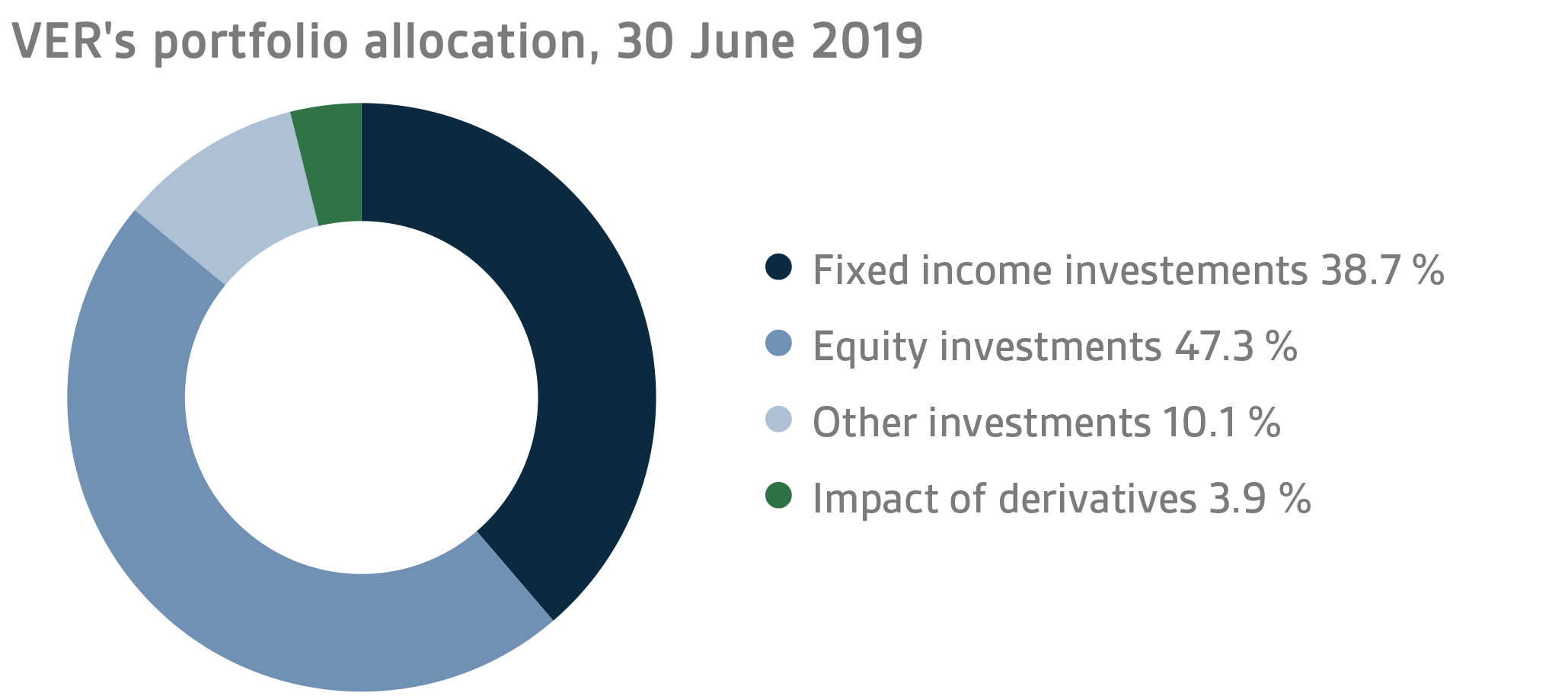

In accordance with the directive of the Ministry of Finance, VER’s investments are divided into fixed income instruments, equities and other investments. At the end of June, fixed income instruments accounted for 38.7 per cent, equities 47.3 per cent and other investments 10.1 per cent. Of the large asset classes, liquid fixed income instruments generated a return of 3.6 per cent and listed equities 14.5 per cent during the first half of the year.

FIXED INCOME INVESTMENTS

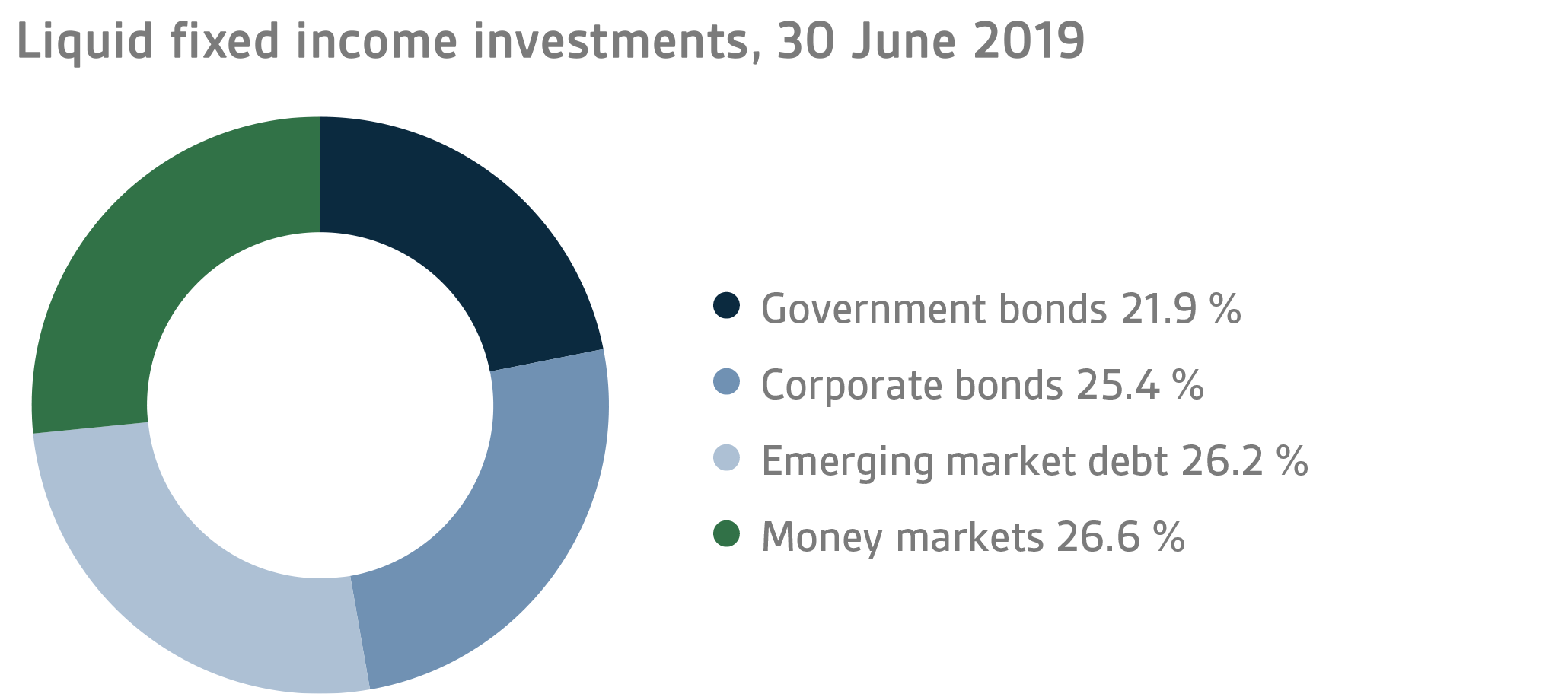

Liquid fixed income investments

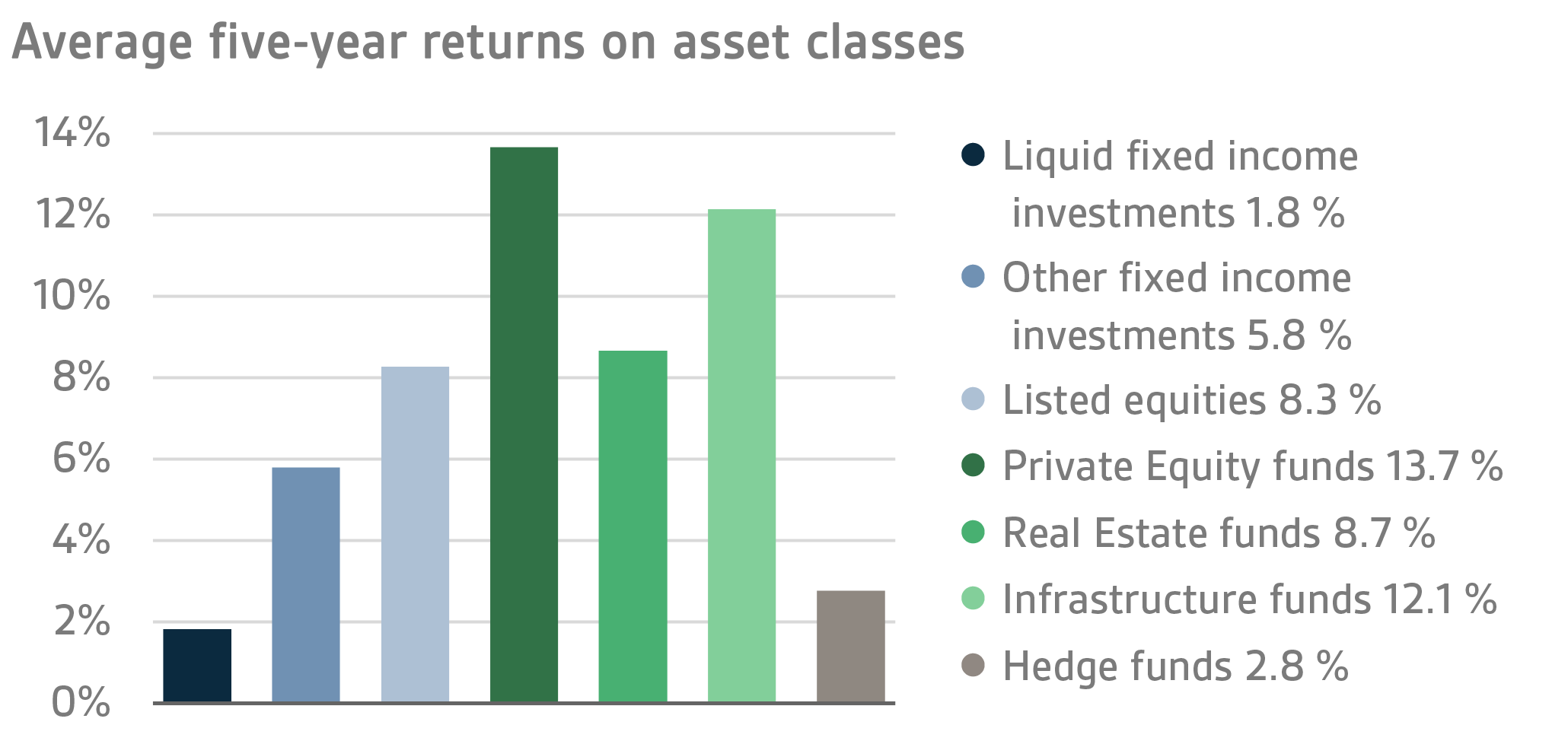

During the first half of the year, the return on liquid fixed income instruments was 3.6 per cent.

In particular, the most risk-filled fixed income investments improved considerably during the first six months relative to their weak performance in 2018. Despite the consistently poor economic data, the risk premiums on emerging debt and corporate loans shrunk substantially and the general interest interest rate levels declined clearly, as central banks gave signals of a more expansionary monetary policy.

At its March rate-setting meeting, the European Central Bank (ECB) announced that it will leave the rates unchanged at least up to the end of 2019, and commence long-term two-year financing operations quarter by quarter in September 2019. Already at its June meeting, the bank had adjusted its policy to maintain current rates at least up to the end of the first half of 2020. At the same time, Draghi underlined the ECB’s willingness to support economic development if so required. The yield on German 10-year government bonds fell to -0.33 per cent at the end of June.

The US Federal Reserve indicated in March that it would not raise its benchmark rate in 2019 and that it would end the reduction of its balance sheet in September. As a number of comments favouring interest rate cuts were heard from the FED during the summer, the markets discounted three 25-point cuts in rates for 2019 and one for 2020. By the end of June, the yield on U.S. 10-year government bonds fell to two per cent.

As a result of the central bank driven interest rate rally, interest index rates increased substantially except for the most short-term rates.

Other fixed income investments

Other fixed income investments include investments in private credit funds and direct lending to companies.

Private credit investments yielded a 0.6 per cent return.

Although a corrective adjustment to the private credit market has been expected for a long time, investor interest in this asset class does not seem to be declining. Fund raising has been active and fund sizes continue to grow. However, the weakening economic prospects increase the probability of a corrective adjustment as portfolio companies’ financial performance appears to deteriorate.

EQUITIES

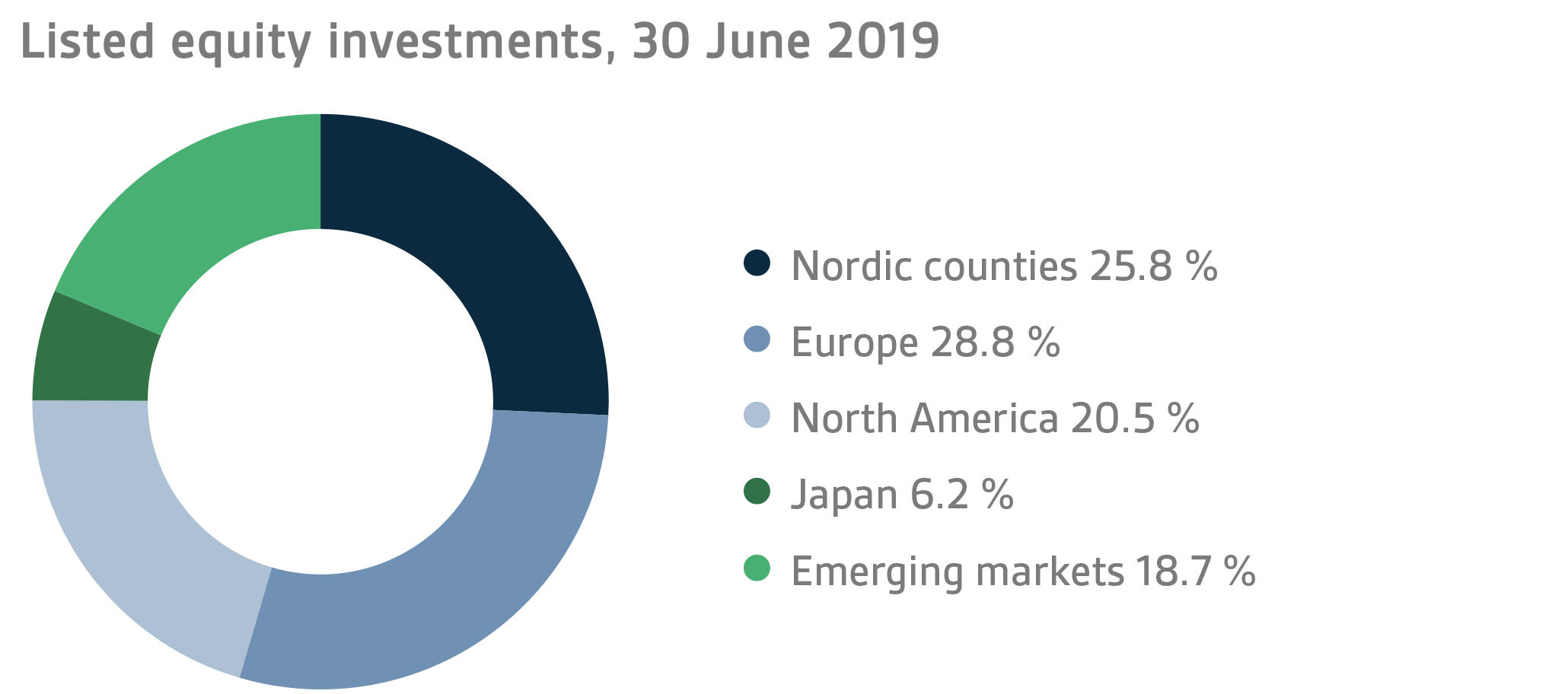

Listed equities

The return on listed equities during the first half of the year was 14.5 per cent.

The first half of 2019 was extremely favourable for the global investment market. Stock prices started rising sharply after the year-end and the great uncertainty felt in the market during the last quarter of 2018 was quickly dispelled. Driven by a strong risk sentiment, the equity market performed well without any major corrections up to the end of April. While one of the main drivers behind the risk sentiment was the increasingly cautious monetary policy position of central banks, there were also reports of progress in the trade talks between the United States and China, which contributed to the positive mood in the financial market. However, the trade talks literally hit the wall in early May, which turned the mood more cautious in one stroke. As a result, global equity prices fell considerably during May. However, the market began to slowly recover in June, partly due to the announcements made by central banks. By the end of the reporting period, the return on equities had reached a very high level.

Other equity investments

VER’s other equity investments include investments in private equity funds, non-listed stock and listed real estate investment trusts (REITs).

Private equity investments returned 5.5 per cent, unlisted equities 2.4 per cent and listed real estate investment trusts 15.3 per cent.

Both equity investments and listed real estate investment funds benefited from the positive development of the stock markets during the first half of the year. So far, the weakening economic prospects have not, however, been reflected in the actual valuation levels of equity investment portfolio companies, nor in debt ratios. But there are growing concerns about the future returns on the funds. With the weakening market, the high purchase prices and debt ratios will be reflected negatively in the fund returns earned by many fund managers.

OTHER INVESTMENTS

VER’s other investments are investments in real estate, infrastructure, hedge funds and risk premium strategies.

The return on unlisted real estate funds was 2.3 per cent while infrastructure investments yielded 6.5 per cent.

No major changes relative to previous developments have so far taken place in the real estate market. However, the returns expected by investors in the individual sectors have diverged. Currently, the overall interest in commercial properties is waning, whereas residential units are attracting more investors.

Underlying the hefty returns on infrastructure funds are extremely skilful exits by some funds. No major changes have so far taken place in the market conditions. The asset class is of interest to investors who seek a continuous cash flow, and so the efforts to raise funding have been relatively successful.

The return on hedge funds during the first half of the year was 4.1 per cent. Most investment styles did well with hedge funds, the biggest returns being earned by macro funds. For volatility funds, the reporting period was more challenging, which was only to be expected as risk-filled investments performed very well.

The return on risk premiums was -0.6 per cent during the first half of the year. For funds relying on conventional risk premium strategies, the first six months was a tough time especially as value strategies proved unsuccessful.

STATE PENSION EXPENDITURE, VER’S TRANSFERS TO THE GOVERNMENT BUDGET, PENSION CONTRIBUTION INCOME AND FUNDING RATIO

The State Pension Fund’s role in balancing government finances has grown and will continue to do so. In 2018, the state’s pension expenditure totalled over EUR 4.6 billion while the 2019 budget foresees an expenditure of nearly EUR 4.8 billion. As VER contributes 40 per cent towards these expenses to the government budget, the transfer to the 2019 budget will amount to about EUR 1.9 billion. By the end of June, VER had transferred EUR 952 million to the government budget.

During the first half of the year, VER’s pension contribution income totalled EUR 680 million. As of the beginning of 2019, billing for pension contributions is based on the pay information saved in the Income Register. However, as the deployment of the Income Register has been beset by problems throughout the first half of the year and all pay data has not been duly recorded in it, part of the pension contribution income due to VER will be billed at a later date. Even without this delay, VER’s net pension contribution income has turned permanently negative, meaning that clearly more money is transferred by VER to the government budget than VER receives in pension contribution income. This gap between income and budget transfers will continue to grow year on year and slow down the growth of the Fund.

In June 2016, the Board of Directors of the State Pension Fund adopted a strategy that defines its long-term objectives in greater detail. The strategy foresees that the 25 per cent funding ratio target specified by law will be attained by 2033, if not earlier. To achieve this, it is imperative that VER’s pension contribution income remains at the estimated level and that the real return on investments remains relatively high. As the state’s pension liabilities amounted to EUR 92.1 billion at the end of 2018, the funding ratio was approx. 20 per cent. Additionally, the strategy set out the principles by which the risk level and basic allocation of the investment portfolio are derived from the target funding ratio established for VER.

KEY FIGURES

|

|

|

| |

30.6.2019

|

31.12.2018

|

|

Investments, MEUR (market value)

|

19 658

|

18 486

|

|

Fixed income investments

|

7 610

|

7 106

|

|

Equity investments

|

9 297

|

8 720

|

|

Other investments

|

1 982

|

1 823

|

|

Impact of derivatives

|

769

|

837

|

| |

|

Breakdown of the investment portfolio

|

|

Fixed income investments

|

38,7 %

|

38,4 %

|

|

Equity investments

|

47,3 %

|

47,2 %

|

|

Other investments

|

10,1 %

|

9,9 %

|

|

Impact of derivatives

|

3,9 %

|

4,5 %

|

| |

| |

1.1.–30.6.2019

|

1.1.–31.12.2018

|

|

Return on investment

|

8,2 %

|

-3,4 %

|

|

Fixed income investments

|

|

Liquid fixed income investments

|

3,6 %

|

-1,9 %

|

|

Other fixed income investments

|

0,6 %

|

8,4 %

|

|

Equity investments

|

|

Listed equity investments

|

14,5 %

|

-7,4 %

|

|

Private Equity investments

|

5,5 %

|

13,4 %

|

|

Listed Real Estate funds

|

15,3 %

|

|

|

Other investments

|

|

Non-listed Real Estate funds

|

2,3 %

|

0,0 %

|

|

Infrastructure funds

|

6,5 %

|

11,2 %

|

|

Hedge funds

|

4,1 %

|

-2,5 %

|

| |

|

Pension contribution income, MEUR

|

680

|

1 425

|

|

Transfer to state budget, MEUR

|

-952

|

-1 859

|

|

Net contribution income, MEUR

|

-272

|

-434

|

|

Pension liability, BnEUR

|

|

92,1

|

|

Funding ratio, %

|

|

20 %

|

Inquiries:

Additional information is provided by CEO Timo Viherkenttä, firstname.lastname@ver.fi, tel.: +358 295 201 210.

Established in 1990, the State Pension Fund (VER) is an off-budget fund through which the state prepares to finance future pensions and equalise pension expenditure. VER is an investment organisation responsible for investing the state’s pension assets professionally. At the end of June 2019, the market value of the Fund’s investment portfolio stood at EUR 19.7 billion.

All figures presented in this interim report are preliminary and unaudited.